Blank Louisiana Cift 620 PDF Form

Blank Louisiana Cift 620 PDF Form

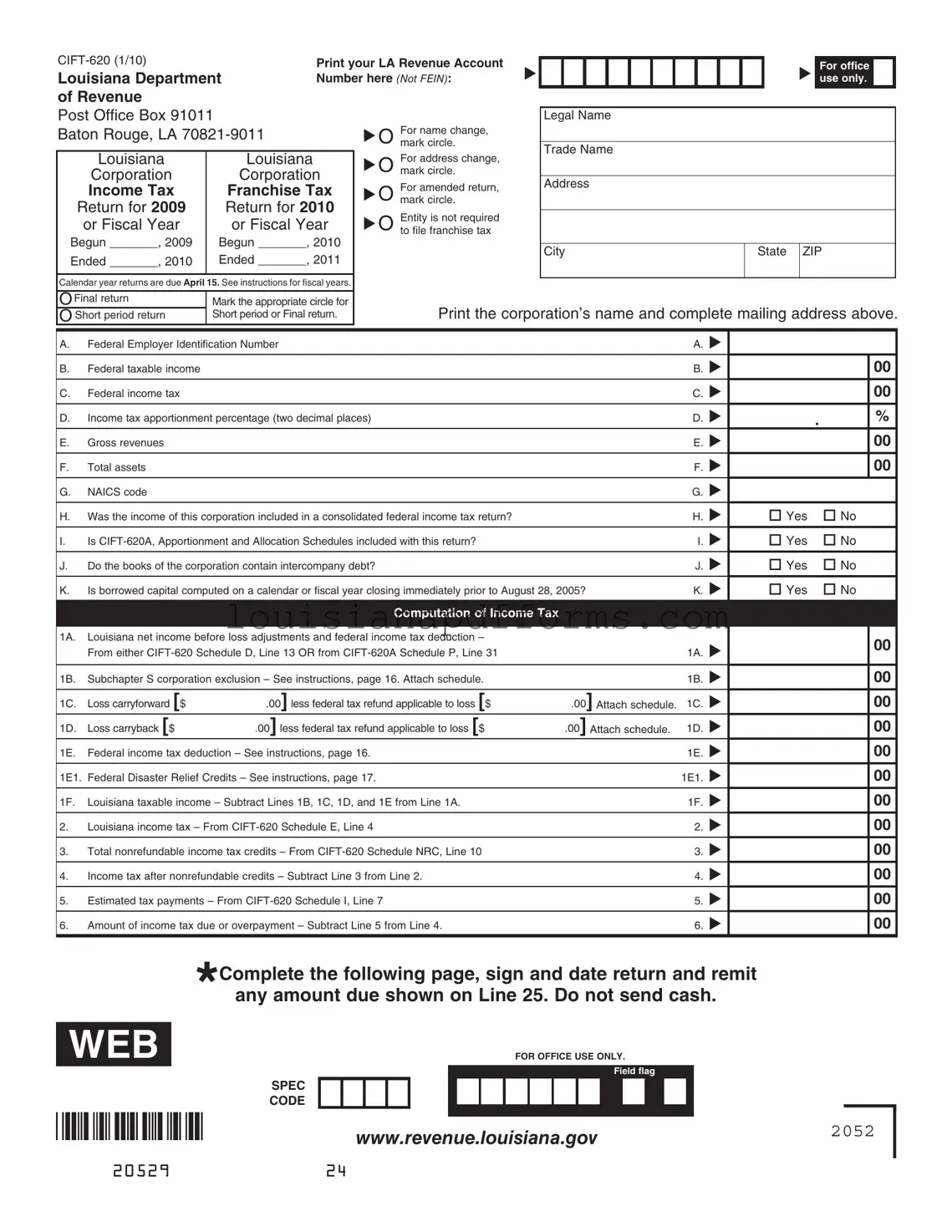

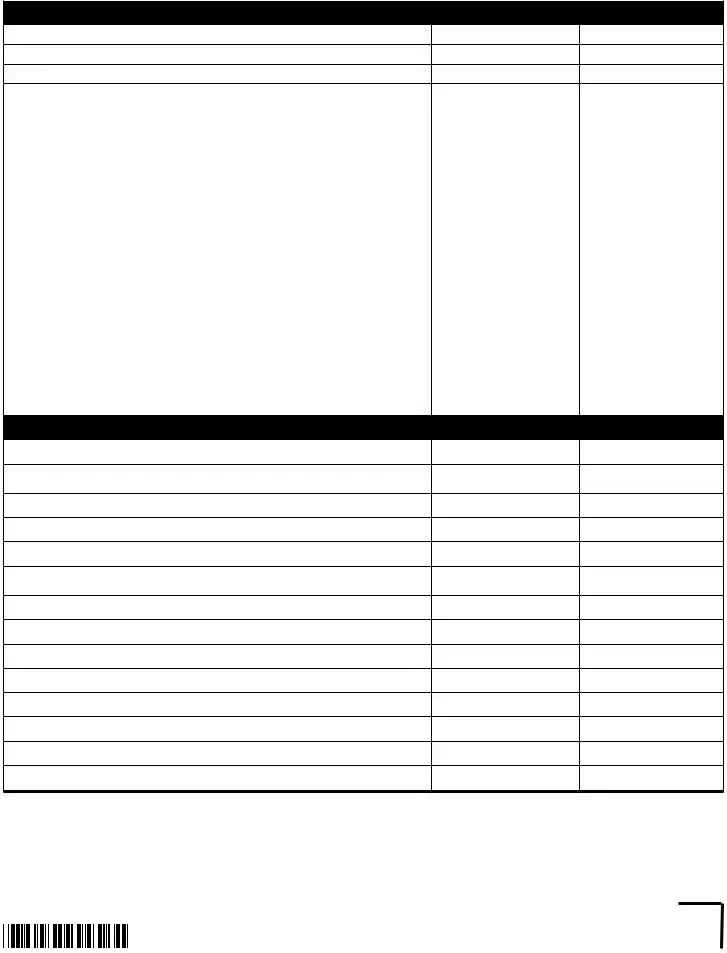

The Louisiana CIFT 620 form is an essential document for corporations operating within the state, as it serves as both the Corporation Income Tax Return and the Corporation Franchise Tax Return. Corporations must complete this form to report their income, calculate their tax liabilities, and determine any applicable credits or deductions. The form includes sections for basic information such as the corporation's legal name, trade name, and federal employer identification number. Additionally, it requires detailed financial data, including federal taxable income, gross revenues, and total assets. Corporations must also indicate their income tax apportionment percentage and provide information regarding any intercompany debt. The form facilitates the computation of both income and franchise taxes, allowing corporations to account for various nonrefundable credits, estimated tax payments, and any overpayments. Furthermore, it includes schedules that require additional disclosures related to assets, liabilities, and tax credits, ensuring a comprehensive overview of the corporation's financial standing. Properly completing the CIFT 620 form is crucial for compliance with Louisiana tax regulations and for accurately determining tax obligations.

Print your LA Revenue Account |

u |

|

|

|

|

|

|

|

|

|

|

|

Louisiana Department |

|

|

|

|

|

|

|

|

|

|

||

Number here (NOT FEIN): |

|

|

|

|

|

|

|

|

|

|

|

|

of Revenue |

|

|

|

|

|

|

|

|

|

|

|

|

u

For office use only.

Post Office Box 91011

Baton Rouge, LA

uO |

For name change, mark circle.

Legal Name

Trade Name

Louisiana

Corporation

Income Tax

Return for 2009

or Fiscal Year

Begun _______, 2009

Ended _______, 2010

Louisiana

Corporation

Franchise Tax Return for 2010 or Fiscal Year

Begun _______, 2010

Ended _______, 2011

uO |

uO |

uO |

For address change, mark circle.

For amended return, mark circle.

Entity is not required to ile franchise tax

Address

City |

State |

ZIP |

|

|

|

Calendar year returns are due April 15. See instructions for iscal years.

OFinal return |

Mark the appropriate circle for |

O Short period return |

Short period or Final return. |

Print the corporation’s name and complete mailing address above.

A. |

Federal Employer Identiication Number |

|

A. u |

|

|

|

||

|

|

|

|

|

|

|

|

|

B. |

Federal taxable income |

|

|

B. u |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

C. |

Federal income tax |

|

|

C. u |

|

|

00 |

|

|

|

|

|

|

|

|

||

D. |

Income tax apportionment percentage (two decimal places) |

|

D. u |

. |

|

% |

||

E. |

Gross revenues |

|

|

E. u |

|

|

00 |

|

F. |

Total assets |

|

|

F. u |

|

|

00 |

|

G. |

NAICS code |

|

|

G. u |

|

|

|

|

|

|

|

|

|

|

|||

H. |

Was the income of this corporation included in a consolidated federal income tax return? |

|

H. u |

o Yes |

o No |

|||

I. |

Is |

|

I. u |

o Yes |

o No |

|||

J. |

Do the books of the corporation contain intercompany debt? |

|

J. u |

o Yes |

o No |

|||

K. |

Is borrowed capital computed on a calendar or iscal year closing immediately prior to August 28, 2005? |

K. u |

o Yes |

o No |

||||

|

|

Computation of Income Tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1A. |

Louisiana net income before loss adjustments and federal income tax deduction – |

|

|

u |

|

|

00 |

|

|

From either |

|

1A. |

|

|

|||

|

|

|

|

|

|

|

|

|

1B. |

Subchapter S corporation exclusion – See instructions, page 16. Attach schedule. |

|

1B. |

u |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

1C. |

Loss carryforward [$ |

.00] less federal tax refund applicable to loss [$ |

.00] Attach schedule. |

1C. |

u |

|

|

00 |

1D. |

Loss carryback [$ |

.00] less federal tax refund applicable to loss [$ |

.00] Attach schedule. |

1D. |

u |

|

|

00 |

1E. |

Federal income tax deduction – See instructions, page 16. |

|

1E. |

u |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

1E1. |

Federal Disaster Relief Credits – See instructions, page 17. |

|

1E1. |

u |

|

|

00 |

|

1F. |

Louisiana taxable income – Subtract Lines 1B, 1C, 1D, and 1E from Line 1A. |

|

1F. |

u |

|

|

00 |

|

2. |

Louisiana income tax – From |

|

2. |

u |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

3. |

Total nonrefundable income tax credits – From |

|

3. |

u |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

4. |

Income tax after nonrefundable credits – Subtract Line 3 from Line 2. |

|

4. |

u |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

5. |

Estimated tax payments – From |

|

5. |

u |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

6. |

Amount of income tax due or overpayment – Subtract Line 5 from Line 4. |

|

6. |

u |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

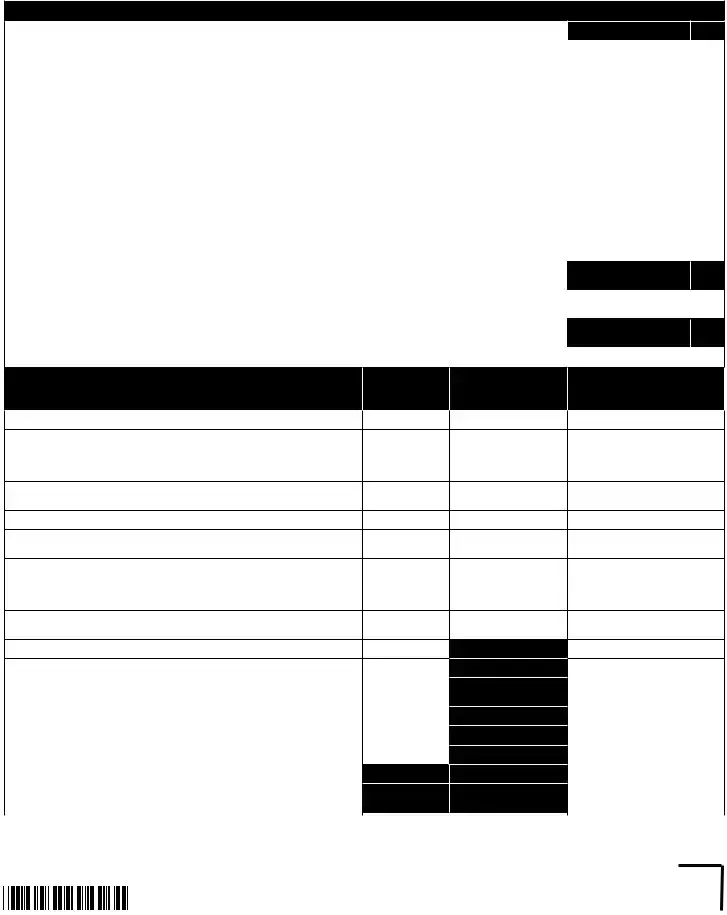

*Complete the following page, sign and date return and remit

any amount due shown on Line 25. Do not send cash.

WEB

FOR OFFICE USE ONLY.

Field lag

SPEC

CODE

www.revenue.louisiana.gov2052

2052924

Print your LA Revenue Account Number here. u _____________________________

Computation of Franchise Tax

7A. |

Total capital stock, surplus, undivided proits, & borrowed capital – From |

7A. |

u |

|

|

|

|

|

|

7B. |

Franchise tax apportionment percentage – From |

|

|

|

|

Percentage must be carried out to 2 decimal places. Do not exceed 100.00%. |

7B. |

u |

. |

|

|

|

|

|

7C. |

Franchise taxable base – Multiply Line 7A by Line 7B. |

7C. |

u |

|

|

|

|

|

|

8. |

Amount of assessed value of real and personal property in Louisiana in 2009 |

8. |

u |

|

|

|

|

|

|

9. |

Louisiana franchise tax – From |

9. |

u |

|

|

|

|

|

|

10. |

Total nonrefundable franchise tax credits – From |

10. |

u |

|

|

|

|

|

|

11. |

Franchise tax after nonrefundable credits – Subtract Line 10 from Line 9. |

11. |

u |

|

|

|

|

|

|

12. |

Previous payments |

12. u |

|

|

|

|

|

|

|

13. |

Amount of franchise tax due or overpayment – Subtract Line 12 from Line 11. |

13. |

u |

|

|

Net Amount Due |

|

|

|

|

|

|

|

|

00

%

00

00

00

00

00

00

00

14. |

Total income and franchise tax due or overpayment – Add Lines 6 and 13. |

14. u |

|

|

|

|

|

15. |

Louisiana Citizens Insurance Credit – See instructions, page 17. |

15. |

u |

|

|

||

15A. Other refundable credits – From |

15A. u |

||

|

|

|

|

15B. Subtotal – Add Lines 15 and 15A and print the result. |

15B. |

u |

|

|

|

|

|

16. |

Net income and franchise taxes overpayment. If Line 14 is equal to Line 15B, print zero on |

|

|

|

Lines 16 through 23 and go to Line 24. If Line 14 is less than Line 15B, subtract Line 14 from |

|

|

|

Line 15B and print the result here. If Line 14 is greater than Line 15B, print zero on Lines 16 |

|

u |

|

through 19 and go to Line 20. – See instructions, page 17. |

16. |

|

17. |

Amount of overpayment you want to donate to The Military Family Assistance Fund |

17. |

u |

|

|

|

|

18. |

Amount of overpayment you want Refunded |

18. u |

|

|

|

|

|

19. |

Amount of overpayment you want Credited to 2010 |

19. u |

|

|

|

|

|

20. |

Amount due – If Line14 is greater than Line 15B, subtract Line 15B from Line 14 and print the result. |

20. |

u |

|

|

|

|

21. |

Delinquent iling penalty – See instructions, page 17. |

21. |

u |

|

|

|

|

22. |

Delinquent payment penalty – See instructions, page 17. |

22. |

u |

|

|

|

|

23. |

Interest – See instructions, page 17. |

23. |

u |

|

|

|

|

24. |

Additional donation to The Military Family Assistance Fund |

24. |

u |

|

|

|

|

25. |

Total amount due – Add Lines 20 through 24. |

25. |

u |

|

Make payment to Louisiana Department of Revenue. DO NOT SEND CASH. |

||

|

|

|

|

|

|

|

|

00

00

00

00

00

00

00

00

00

00

00

00

00

00

Under the penalties of perjury, I declare that I have examined this return, including all accompanying documents, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which he has any knowledge.

Print name of officer

Signature of oficer

Signature of preparer

Firm name

|

( |

) |

|

Title of oficer |

|

|

Telephone |

Date

()

Telephone

Date

WEB |

2053 |

Print your LA Revenue Account Number here. u _____________________________

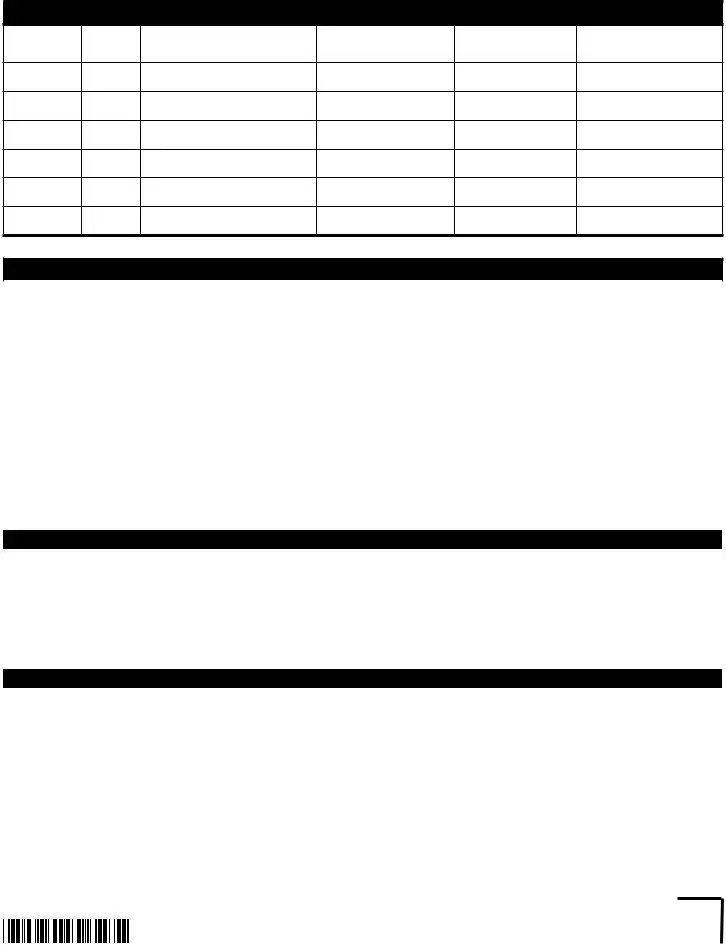

Schedule NRC – Nonrefundable Tax Credits, Exemptions, and Rebates

|

Description |

|

Code |

Corporation |

|

Corporation |

||

|

|

|

|

|

Franchise Tax (B) |

|||

|

|

|

|

Income Tax (A) |

|

|||

|

|

|

|

|

|

|

|

|

1. |

|

u |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

2. |

|

u |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

3. |

|

u |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

4. |

|

u |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

5. |

|

u |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

6. |

|

u |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

7. |

|

u |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

8. |

|

u |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

9. |

|

u |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

10. |

Total Income Tax Credits: Add credit amounts in Column A. Print here and on |

|

|

00 |

|

|

||

|

|

|

|

|

|

|

||

11. |

Total Franchise Tax Credits: Add credit amounts in Column B. Print here and on |

|

|

|

|

00 |

||

|

|

|

|

|

|

|

|

|

For further information about these credits, please see instructions beginning on page 18.

Description |

Code |

|

Premium Tax |

100 |

|

|

|

|

Bone Marrow |

120 |

|

|

|

|

Nonviolent Offenders |

140 |

|

|

|

|

Qualiied Playgrounds |

150 |

|

|

|

|

Debt Issuance |

155 |

|

|

|

|

Contributions to |

160 |

|

Educational Institutions |

||

|

||

Donations to |

170 |

|

Public Schools |

||

|

Description |

Code |

Donations of Materials, |

|

Equipment, Advisors, |

175 |

Instructors |

|

Other |

199 |

|

|

Atchafalaya Trace |

200 |

|

|

Previously Unemployed |

208 |

|

|

Recycling Credit |

210 |

|

|

Basic Skills Training |

212 |

|

|

Dedicated Research |

220 |

|

|

New Jobs Credit |

224 |

|

|

Refunds by Utilities |

226 |

|

|

Description |

Code |

|

Eligible |

228 |

|

Neighborhood Assistance |

230 |

|

|

|

|

Cane River Heritage Area |

232 |

|

|

|

|

La Community Economic Dev |

234 |

|

Apprenticeship |

236 |

|

|

|

|

Ports of Louisiana Investor |

238 |

|

|

|

|

Ports of Louisiana Import |

240 |

|

Export Cargo |

||

|

||

Motion Picture Investment |

251 |

|

Research and Development |

252 |

|

|

|

|

Historic Structures |

253 |

|

|

|

|

Digital Interactive Media |

254 |

Description |

Code |

Motion Picture Resident |

256 |

Capital Company |

257 |

LCDFI Credit |

258 |

New Markets |

259 |

Brownields Investor |

260 |

Motion Picture Infrastructure |

261 |

Other |

299 |

Biomed/University Research |

300 |

Tax Equalization |

305 |

Manufacturing Establishments |

310 |

Enterprise Zone |

315 |

Other |

399 |

Schedule RC – Refundable Tax Credits and Rebates

|

Description |

|

Code |

Amount of Credit Claimed |

|

|

|

|

|

|

|

1. |

|

u |

F |

|

00 |

|

|

|

|

|

|

2. |

|

u |

F |

|

00 |

|

|

|

|

|

|

3. |

|

u |

F |

|

00 |

|

|

|

|

|

|

4. |

|

u |

F |

|

00 |

|

|

|

|

|

|

5. |

|

u |

F |

|

00 |

|

|

|

|

|

|

6. |

Total: Add lines 1 through 5. Print the result here and on Line 15A. |

u |

|

|

00 |

|

|

|

|

|

|

For further information about these credits, please see instructions beginning on page 20.

Description |

Code |

|

Inventory Tax |

50F |

|

Ad Valorem Natural Gas |

51F |

|

Ad Valorem Offshore Vessels |

52F |

|

Telephone Company |

54F |

|

Property |

||

|

||

|

|

|

Prison Industry Enhancement |

55F |

|

|

|

|

Urban Revitalization |

56F |

Description |

Code |

|

57F |

||

|

|

|

Milk Producers |

58F |

|

|

|

|

Technology |

59F |

|

Commercialization |

||

|

||

Angel Investor |

61F |

|

|

|

|

Musical and Theatrical |

62F |

|

Production |

||

|

||

|

|

Description |

Code |

|

Wind and Solar Energy |

64F |

|

Systems |

||

|

||

|

|

|

School Readiness Child |

65F |

|

Care Provider |

||

|

||

|

|

|

School Readiness Business |

67F |

|

- Supported Child Care |

|

|

School Readiness Fees |

|

|

and Grants to Resource |

68F |

|

and Referral Agencies |

|

Description |

Code |

|

Sugarcane Trailer Conversion |

69F |

|

|

|

|

Retention and Modernization |

70F |

|

|

|

|

Conversion of Vehicle to |

71F |

|

Alternative Fuel |

||

|

||

Research and Development |

72F |

|

|

|

|

Other Refundable |

80F |

|

|

|

WEB2054

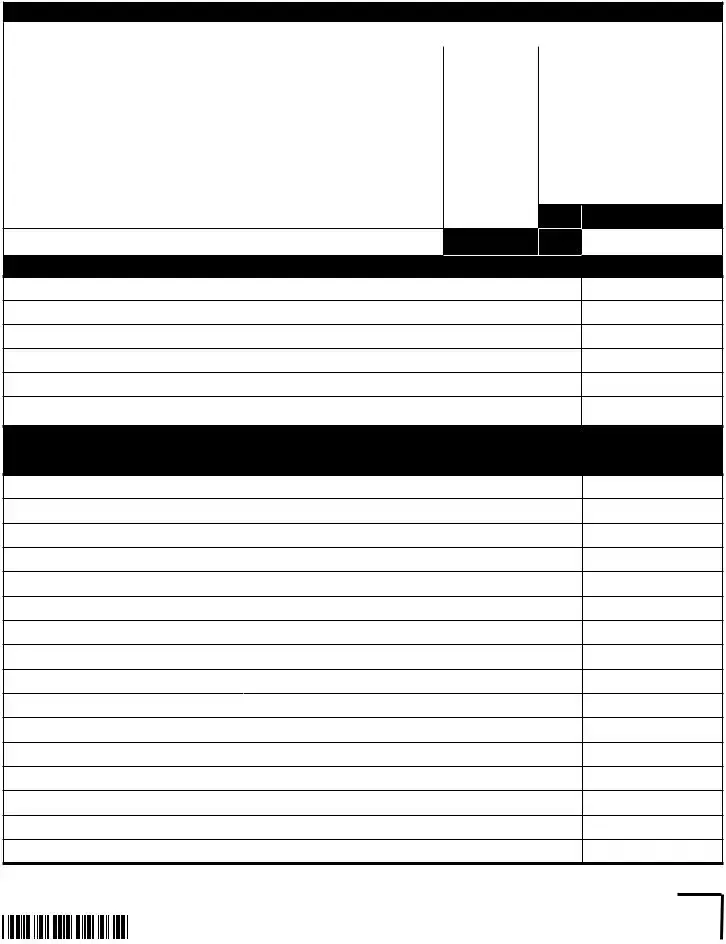

Print your LA Revenue Account Number here. u _____________________________

All applicable schedules must be completed.

Schedule A – Balance Sheet

ASSETS |

1. Beginning of year |

2. End of year |

1.Cash

2.Trade notes and accounts receivable

3. |

Reserve for bad debts |

( |

) |

( |

) |

4. |

Inventories |

|

|

|

|

|

|

|

|

|

|

5. |

Investment in United States government obligations |

|

|

|

|

|

|

|

|

|

|

6. |

Other current assets – Attach schedule. |

|

|

|

|

|

|

|

|

|

|

7. |

Loans to stockholders |

|

|

|

|

|

|

|

|

|

|

8. |

Stock and obligations of subsidiaries |

|

|

|

|

|

|

|

|

|

|

9. |

Other investments – Attach schedule. |

|

|

|

|

|

|

|

|

|

|

10. Buildings and other ixed depreciable assets |

|

|

|

|

|

|

|

|

|

|

|

11. Accumulated amortization and depreciation |

( |

) |

( |

) |

|

12. Depletable assets |

|

|

|

|

|

|

|

|

|

|

|

13. Accumulated depletion |

( |

) |

( |

) |

|

14. Land |

|

|

|

|

|

|

|

|

|

|

|

15. Intangible assets |

|

|

|

|

|

|

|

|

|

|

|

16. Accumulated amortization |

( |

) |

( |

) |

|

17. Other assets – Attach schedule. |

|

|

|

|

|

|

|

|

|

|

|

18. Excessive reserves or undervalued assets – Attach schedule. |

|

|

|

|

|

|

|

|

|

|

|

19. Totals – Add Lines 1 through 18. |

|

|

|

|

|

Liabilities and Capital

20. Accounts payable

21. Mortgages, notes, and bonds payable one year old or less at balance sheet date and having a maturity of one year or less from original date incurred

22. Other current liabilities – Attach schedule.

23. Loans from stockholders – Attach schedule.

24. Due to subsidiaries and affiliates

25. Mortgages, notes, and bonds payable more than one year old at balance sheet date or having a maturity of more than one year from original date incurred

26. Other liabilities – Attach schedule.

27. Capital stock: a. Preferred stock

b. Common stock

28.

29. Surplus reserves – Attach schedule.

30. Earned surplus and undivided proits

31. Excessive reserves or undervalued assets

32. Totals – Add Lines 20 through 31.

WEB |

2055 |

Print your LA Revenue Account Number here. u _____________________________

For Schedule

All applicable schedules must be completed. Complete lines 1 through 11 only if there is an end of year balance in the “Due to Subsidiaries and Affiliates” account or an equivalent account on the books of the corporation.

Schedule

1. Capital Stock:

1A. |

Common Stock – Include |

|

|

00 |

|

|

|

|

|

1B. |

Preferred Stock – Include |

|

|

00 |

2. Total Capital stock – Add Lines 1A and 1B. |

|

|

00 |

|

|

|

|

|

|

3. Surplus and undivided proits |

|

|

00 |

|

|

|

|

|

|

4. Surplus reserves – Include any excessive reserves or undervalued assets. |

|

|

00 |

|

|

|

|

|

|

5. Total – Add Lines 2, 3, and 4. |

|

|

00 |

|

|

|

|

|

|

6. Due to subsidiaries and affiliates |

|

|

00 |

|

7. Deposit liabilities to affiliates – Included in the amount on Line 6 |

|

|

00 |

|

|

|

|

|

|

8. Accounts payable less than 180 days old – Included in the amount on Line 6 |

|

|

00 |

|

|

|

|

|

|

9. Adjusted debt to affiliates – Subtract Lines 7 and 8 from Line 6. |

|

|

00 |

|

|

|

|

||

10A. If Line 9 above is greater than zero, AND Line 5 above is greater than or equal to zero, subtract Line 5 |

|

00 |

||

from line 9. If both conditions of this line do not apply, skip to Line 10B. |

|

|

||

|

|

|

||

|

|

|

||

10A1. If Line 10A is less than zero, print zero on Line 11 and Line 24, column 3. If Line 10A is greater than zero, |

|

|

||

multiply Line 10A by 50% and print this amount on Line 11 and Line 24, column 3. |

|

|

|

|

|

|

|

||

10B. If Line 9 is greater than zero, AND Line 5 is less than or equal to zero, subtract Line 5 from Line 9. |

|

00 |

||

Multiply the difference by 50% and print the result here. |

|

|

||

|

|

|

||

10B1. Print the lesser of Line 9 or Line 10B on Line 11 and Line 24, column 3. If Line 9 equals Line 10B, print that |

|

|

||

amount on Line 11 and on Line 24, column 3. |

|

|

|

|

11. Print the amount from either Line 10A1 or 10B1. |

|

|

00 |

|

|

1 |

2 |

3 |

|

|

End of year |

70% reduction |

Total |

|

|

|

for items of debt |

(See note below.) |

|

|

|

|

|

|

12.Accounts payable

13.Mortgages, notes and bonds payable one year old or less at balance sheet date and having a maturity of one year or less from original date incurred. – Complete Schedule B. Do Not include indebtedness from the Louisiana Infrastructure Bank.

14.Other current liabilities – Attach Schedule.

Do Not include items of surplus. See RIB

15.Loans from stockholders – Attach Schedule.

16.End of year balance due to subsidiaries and affiliates, less amount on Line 11. If less than zero, print zero.

17.Mortgages, notes and bonds payable more than one year old at balance sheet date or having a maturity of more than one year from original date incurred. – Do Not include indebtedness from the Louisiana Infrastructure Bank.

18.Other liabilities – Attach schedule.

Do Not include items of surplus. See RIB

19.Capital Stock: Common Stock

|

|

Preferred Stock |

|

|||||

|

|

|

|

|

|

|

|

|

20. |

|

|||||||

|

|

of par value. |

|

|

|

|||

21. |

Surplus reserves – Attach schedule. |

|

||||||

|

|

|

|

|

|

|

|

|

22. |

Earned surplus and undivided proits |

|

||||||

|

|

|

|

|

|

|

|

|

23. |

Excess reserves or undervalued assets |

|

||||||

|

|

|

|

|

|

|

|

|

24. |

Additional surplus and undivided proits – From Line 11 above |

|

||||||

|

|

|

|

|

|

|

||

|

25. Total – Add the amounts in Column 3, Lines 12 through 24. Print the total in |

|

||||||

|

|

Column 3 and on |

|

|||||

Note: Print in Column 1 those items that are included in the franchise taxable base. Multiply Lines 12 through 18 by the percentage |

|

|||||||

|

of reduction in Column 2. Subtract the result from Column 1 and print the amount in Column 3. |

|

||||||

|

|

|

|

|

||||

|

|

|

WEB |

|

2056 |

|||

|

|

|

|

|

|

|

|

|

Print your LA Revenue Account Number here. u _____________________________

All applicable schedules must be completed.

Schedule B – Analysis of Schedule A1, Column 1, Lines 13, 15, and 18

Original date of inception

Due date

Payee

Installment amount

Balance due

Taxable amount

Schedule C – Analysis of Schedule A, Line 30, Column 2 – Earned surplus and undivided profits per books

1. |

Balance at beginning of year |

|

5. Distributions: |

a. Cash |

|

|

|

|

|

|

|

|

|

|

|

2. |

Net income per books |

|

|

b. Stock |

|

|

|

|

|

|

|

|

|

|

|

3. |

Other increases – Itemize. |

|

|

c. Property |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6. Other decreases – Itemize. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7. Total – Add Lines 5 and 6. |

|

|

|

|

|

|

|

|

|

||

4. |

Total – Add Lines 1, 2, and 3. |

|

8. Balance at end of year – Subtract Line 7 from Line 4. |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

Schedule D – Computation of Louisiana Taxable Income |

|

|

||

|

|

Schedule D need not be completed if Form |

|||||

|

|

|

|

|

|

|

|

1. |

|

Federal taxable income |

|

|

1. |

|

|

|

|

|

|

|

|

||

|

|

|

Additions to Federal Taxable Income |

|

|

||

|

|

|

|

|

|

|

|

2. |

|

Net operating loss deduction claimed on federal return |

|

|

2. |

|

|

|

|

|

|

|

|

|

|

3. |

|

Dividends received deduction claimed on federal return |

|

|

3. |

|

|

|

|

|

|

|

|

|

|

4. |

|

Louisiana income tax deducted on federal return |

|

|

4. |

|

|

|

|

|

|

|

|

|

|

5. |

|

Other additions to federal taxable income – Attach schedule. |

|

|

5. |

|

|

|

|

|

|

|

|

|

|

6. |

|

Total additions – Add Lines 2 through 5. |

|

|

6. |

|

|

|

|

|

|

|

|

||

|

|

|

Subtractions from Federal Taxable Income |

|

|

||

|

|

|

|

|

|

|

|

7. |

|

Refunds of Louisiana income tax reported on federal return |

|

|

7. |

|

|

|

|

|

|

|

|

||

8. |

|

Louisiana depletion in excess of federal depletion – Attach schedule. |

|

8. |

|

||

|

|

|

|

|

|||

9. |

|

Expenses not deducted on the federal return due to Internal Revenue Code Section 280(C) |

9. |

|

|||

|

|

|

|

|

|||

10. |

Road Home – The amount included in federal taxable income. |

|

10. |

|

|||

|

|

|

|

|

|

||

11. |

Other subtractions – Attach schedule. |

|

|

11. |

|

||

|

|

|

|

|

|

||

12. |

Total subtractions – Add Lines 7 through 11. |

|

|

12. |

|

||

|

|

|

|

||||

13. |

Louisiana net income before S corporation exclusion, loss adjustments, and federal income tax deduction – |

|

|

||||

|

|

Add the amount on Line 1 to the amount on Line 6, and subtract the amount on Line 12. Round to the |

13. |

|

|||

|

|

nearest dollar. Print here and on |

|

|

|

|

|

WEB |

2057 |

|

Print your LA Revenue Account Number here. u _____________________________

All applicable schedules must be completed.

Schedule E – Calculation of Income Tax

1. Print the amount of net taxable income from |

|

|

|

|

|

|

|

|

|

|

Column 1 |

|

Column 2 |

|

2. Calculation of tax |

Net income |

RATE |

||

TAX |

||||

|

in each bracket |

|

||

|

|

|

||

|

|

|

|

|

a. First $25,000 of net income |

|

x 4% = |

|

|

|

|

|

|

|

b. Next $25,000 |

|

x 5% = |

|

|

|

|

|

|

|

c. Next $50,000 |

|

x 6% = |

|

|

|

|

|

|

|

d. Next $100,000 |

|

x 7% = |

|

|

|

|

|

|

|

e. Over $200,000 |

|

x 8% = |

|

|

|

|

|

|

3.Add the amounts in Column 1, Lines 2a through 2e and print the result.

4.Add the amounts in Column 2, Lines 2a through 2e. Round to the nearest dollar. Print in Column 2 and on

Schedule F – Calculation of Franchise Tax

1.Print the amount from

2.Print the amount of Line 1 or $300,000, whichever is less.

3.Multiply the amount on Line 2 by $1.50 for each $1,000 or major fraction and print the result.

4.Subtract Line 2 from Line 1 and print the result.

5.Multiply the amount on Line 4 by $3.00 for each $1,000 or major fraction and print the result.

6.Add Lines 3 and 5. Round to the nearest dollar. Print the result here and on

Schedule G – Reconciliation of Federal and Louisiana Net Income

Schedule G is required if Form

Important! See R.S. 47:287.71 and R.S. 47:287.73 for information.

1.Print the total net income calculated under federal law before special deductions.

2.Additions to federal net income: a. Louisiana income tax

b.

c.

d.

e.

f.

Subtractions from federal net income:

a.Dividends

b.Interest

c.Road Home – The amount included in federal taxable income

3.Louisiana net income from all sources – The amount should agree with Form

WEB |

2058 |

|

Print your LA Revenue Account Number here. u _____________________________ |

|

All applicable schedules must be completed. |

||

|

Schedule H – Reconciliation of Income Per Books with Income Per Return |

|

|

|

|

1. Net income per books |

|

7. Income recorded on books this year, but not |

|

|

included in this return – Itemize. |

2. Louisiana income tax |

|

|

3. Excess of capital loss over capital gains |

|

|

|

|

|

|

|

|

|

4. Taxable income not recorded on books this |

|

|

|

|

year – Itemize. |

|

|

|

|

|

|

|

8. Deductions in this tax return not charged |

|

|

|

|

|

|

|

|

|

|

against book income this year: |

|

|

|

|

|

|

|

|

|

a. Depreciation |

|

|

|

|

|

|

|

|

|

b. Depletion |

|

|

|

|

|

5. Expenses recorded on books this year, but not |

c. Other |

|||

|

||||

deducted in this return: |

|

|

|

|

|

|

|

|

|

a. Depreciation |

|

|

|

|

|

|

|

|

|

b. Depletion |

|

|

|

|

|

|

|

|

|

c. Other |

|

|

|

|

|

|

|

|

|

|

|

|

|

9. Total – Add Lines 7 and 8. |

|

|

|

|

|

|

|

|

|

10. Net income from all sources per return – |

6. Total – Add Lines 1 through 5. |

|

|

|

Subtract Line 9 from Line 6. |

|

|

|

|

|

|

|

|

|

|

|

Schedule I – Summary of Estimated Tax Payments |

|||

Check number |

Date |

Amount |

1.Credit from prior year return

2.First quarter estimated payment

3.Second quarter estimated payment

4.Third quarter estimated payment

5.Fourth quarter estimated payment

6.Payment made with extension request

7. Total

Additional Information Required

1.Indicate principal place of business. ___________________________

2.Describe the nature of your business activity and specify your principal product or service, both in Louisiana and elsewhere.

Louisiana:

Elsewhere:

3.Indicate the date and state of incorporation. ____________________

4.Indicate parishes in which property is located.

5.At the end of the tax year, did you directly or indirectly own 50% or more of the voting stock of any corporation or an interest of any part- nership, including any entity treated as a corporation or partnership?

o Yes o No

If “yes,” show name, address, and percentage owned.

6.At the end of the tax year, did any corporation, individual, partnership, trust, or association directly or indirectly own 50% or more of your vot-

ing stock? o Yes o No

If “yes,” show name, address, and percentage owned.

WEB |

2059 |

|

Corporation Apportionment and Allocation Schedules |

|

COMPLETE ALL APPLICABLE SCHEDULES. |

Print your LA Revenue Account Number here. u ___________________________________ |

Name as shown on

Income taxable period covered

Schedule M - Computation of Corporate Franchise Tax and Income Tax Property Ratios

|

|

|

|

Located in Louisiana |

|

|

|

Located everywhere |

Franchise tax |

Income tax property factor |

|||

|

|

|

property factor |

|||

|

|

|

|

|

|

|

1. Items |

2. Beginning of year |

3. End of year |

4. End of year |

5. Beginning of year |

|

6. End of year |

Intangible assets

1.Cash.........................................................

2.Notes and accounts receivable................

3. Reserve for bad debts |

( |

) ( |

) ( |

) |

4.Investment in U.S. govt. obligations.........

5.Stock and obligations of subsidiaries.......

6.Other investments – Attach schedule. .....

7.Loans to stockholders ..............................

8.Other intangible assets – Attach schedule.

9. Accumulated depreciation |

( |

) ( |

) ( |

) |

10. Total intangible assets – Add Lines

|

Real and tangible assets |

|

|

|

|

|

|

|

|

|

|

11. |

Inventories |

|

|

|

|

|

|

|

|

|

|

12. |

Bldgs. and other depreciable assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

13. |

Accumulated depreciation |

|

|

|

|

|

|

|

|

|

|

( |

) |

( |

) |

( |

) |

( |

) |

( |

) |

||

14. |

Depletable assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

15. |

Accumulated depletion |

|

|

|

|

|

|

|

|

|

|

( |

) |

( |

) |

( |

) |

( |

) |

( |

) |

||

16. |

Land |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

17. |

Other real & tangible assets – Attach sch. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

18. |

Excessive reserves, assets not relected |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

on books, or undervalued assets |

|

|

|

|

|

|

|

|

|

|

19. |

Total real and tangible assets – |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Add Lines 11 through 18 |

|

|

|

|

|

|

|

|

|

|

20. |

Total assets – Add Lines 10 and 19 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

21. |

Print the amount from Line 19 above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

22. |

Less real and tangible assets not used |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

in production of net apportionable income |

|

|

|

|

|

|

|

|

|

|

|

– Attach schedule |

|

|

|

|

|

|

|

|

|

|

23. |

Balance |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

24. |

Beginning of year balance |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

25. |

Total – Add Lines 23 and 24 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|||

26. Franchise tax property ratio (Line 20, Column 4 ÷ Line 20, Column 3) |

............................ |

|

__ __ __ . __ __ % |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

27. Income tax property ratio (Line 25, Column 6 ÷ Line 25, Column 3) ..........................................................................................................

Schedule N - Computation of Corporate Franchise Tax Apportionment Percentage

__ __ __ . __ __ %

1. Description of items used as ratios |

2. Total amount 3. Louisiana amount 4. Percent (Col. 3 ÷ Col. 2) |

|

1. Net sales of merchandise, charges for services, and other revenues |

|

|

A. Sales – See instructions, page 24 |

|

|

B. Charges for services – See instructions, page 24 |

|

|

C. Other Revenues – See instructions, page 24.

(i) |

Rents and royalties |

|

For Manufacturers |

|||

This is your apportionment ratio. Print |

||||||

(ii) |

Dividends and interest from subsidiaries |

|

||||

here and on Page 2, Line 7B of |

||||||

(iii) |

Other dividends and interest |

Do NOT proceed further. |

||||

|

|

|

▼ |

|

||

(iv) All other revenues |

|

|||||

D. Total – Add the amounts in Columns 2 and 3. Calculate the ratio and |

|

|

|

|||

print the result in Column 4. For taxpayers whose primary business is |

|

__ __ __ . __ __ % |

|

|||

. ..manufacturing, use this apportionment ratio. See instructions, page 24 |

|

|

||||

2. Franchise tax property ratio – Print in Column 4 the percentage from Schedule M, Line 26 |

__ __ __ . __ __ % |

|

||||

...........................................................................................................................3. Total of applicable percents in Column 4 |

__ __ __ . __ __ % |

|

||||

4. Average of percents – Divide Line 3 by applicable number of ratios. Print here and on |

|

|

||||

__ __ __ . __ __ % |

|

|||||

WEB

2060

Print your LA Revenue Account Number here. u _____________________________

Schedule P - Computation of Louisiana Net Income

Column 3 must be completed. Column 2 must also be completed if the separate accounting method is used.

Those corporations employing the separate accounting method should review R.S. 47:287.94H for guidance. |

2. LA amounts |

3. Totals |

|

1. Items |

(Lines 1 through 25) |

||

|

1.Gross receipts ______________________ Less returns and allowances _______________

2.Less: Cost of goods sold and/or operations – Attach schedules. ........................................................................

3.Gross proit ...........................................................................................................................................................

4.Gross rents ...........................................................................................................................................................

5.Gross royalties ......................................................................................................................................................

6.Income from estates, trusts, partnerships.............................................................................................................

7.Income from construction, repair, etc. ..................................................................................................................

8.Other income – Attach schedule. .........................................................................................................................

9.Total income – Add Lines 3 through 8.............................................................................................................................................

10. Compensation of officers .....................................................................................................................................

11. Salaries and wages (not deducted elsewhere).....................................................................................................

12. Repairs – Do not include cost of improvements or capital expenditures. ............................................................

13. Bad debts..............................................................................................................................................................

14. Rent ......................................................................................................................................................................

15. Taxes – Attach schedule. .....................................................................................................................................

16. Interest ..................................................................................................................................................................

17. Contributions.........................................................................................................................................................

18.Depreciation – Attach schedule. ...........................................................................................................................

19.Depletion – Attach schedule. ................................................................................................................................

20.Advertising ............................................................................................................................................................

21.Pension, proit sharing, stock bonus, and annuity plans ......................................................................................

22.Other employee beneit plans...............................................................................................................................

23.Other deductions – Attach schedule.....................................................................................................................

24.Total deductions – Add Lines 10 through 23........................................................................................................

25.Net income from Louisiana sources – If separate (direct) method of reporting is used, print here and on Line 31.

26.Net income from all sources – Subtract Column 3, Line 24 from Column 3, Line 9. ..........................................

27.Allocable income from all sources – See instructions, page 25. Attach schedule supporting each amount.

A.Net rents and royalties from immovable or corporeal movable property .........................................................

B.Royalties from the use of patents, trademarks, etc. – See instructions, page 25............................................

C.Income from estates, trusts, and partnerships .................................................................................................

D.Income from construction, repair, etc. – See instructions, page 25.................................................................

E.Other allocable income.......................................................................................................................................

28.Net income subject to apportionment – Subtract Lines 27A through 27E from Line 26, Column 3. ...................

29.Net income apportioned to Louisiana – See instructions, page 25. .....................................................................

30.Allocable income from Louisiana sources – See instructions, page 26. Attach schedule supporting each amount.

A.Net rents and royalties from immovable or corporeal movable property .........................................................

B.Royalties from the use of patents, trademarks, etc. – See instructions, page 26............................................

C.Income from estates, trusts, and partnerships .................................................................................................

D.Income from construction, repair, etc. – See instructions, page 26.................................................................

E.Other allocable income.....................................................................................................................................

31.Louisiana net income before loss adjustments and federal income tax deduction –

Add Column 3, Line 29 to Column 2, Lines 30A through 30E. Print the result or the amount on Line 25,

whichever is applicable, here and on Form

Schedule Q - Computation of Income Tax Apportionment Percentage

1. Description of items used as ratios |

2. Total amount 3. Louisiana amount |

4. Percent (Col. 3 ÷ Col. 2) |

|

1. Net sales of merchandise and/or charges for services |

|

For Manufacturers or Merchandisers. |

|

A. Sales – See instructions, page 26 |

|

This is your apportionment ratio. Use this |

|

|

result in determining income apportioned |

||

B. Charges for services – See instructions, page 26 |

|

||

|

to Louisiana on Line 29, Sch. P above. Do |

||

C. Other gross apportionable income |

|

NOT proceed further. |

|

|

|

|

|

D.Total – Add the amounts in Columns 2 and 3. Calculate the ratio and print the result in Column 4. For taxpayers whose primary business is manufacturing

or merchandising, use this apportionment ratio. See instructions, page 26 |

__ __ __ . __ __ % |

2.Wages, salaries, and other personal service compensation paid

|

during the year – Print the amounts in Column 2 and Column 3. |

|

|

|

__ __ __ . __ __ % |

|

Calculate the ratio and print the result in Column 4 |

|

3. |

Income tax property ratio – Print percentage from Schedule M, Line 27 |

__ __ __ . __ __ % |

4. |

Total of percents in Column 4 |

__ __ __ . __ __ % |

5. Average of percents – Multiply this result by the amount on Schedule P, Line 29 to determine the amount of Louisiana apportionable income. |

__ __ __ . __ __ % |

|

|

WEB |

|

|

|

2061 |

When filling out the Louisiana CIFT 620 form, there are several important guidelines to follow. Below is a list of actions to take and avoid:

Louisiana Department of Motor Vehicles Forms - Documentation must be retained for future reference and verification if necessary.

A Durable Power of Attorney (DPOA) is a legal document that allows you to designate someone to make decisions on your behalf if you become incapacitated. In Arizona, this form is essential for ensuring your financial and medical matters are handled according to your wishes. For those looking to understand how to properly complete and execute this document, you can find a helpful resource at https://arizonapdfs.com/durable-power-of-attorney-template, which is crucial for protecting your interests.

2022 Form 540 - Taxpayers must provide Social Security numbers for themselves and their dependents.

Filling out the Louisiana CIFT 620 form is an essential step for corporations to report their income and franchise taxes. To ensure accuracy and compliance, follow the steps outlined below carefully. Each section of the form requires specific information, so gather all necessary documents before you begin.

The Louisiana CIFT 620 form is an essential document for corporations filing income and franchise taxes in Louisiana. Along with this form, several other documents may be required to ensure compliance with state tax regulations. Here’s a list of forms that are often used in conjunction with the CIFT 620, along with a brief description of each.

Each of these forms plays a vital role in accurately reporting a corporation's financial situation and tax obligations in Louisiana. Ensuring all relevant documents are completed and submitted correctly can help avoid delays and penalties. Always consider consulting a tax professional for guidance tailored to your specific circumstances.

The Louisiana CIFT 620 form is a tax return specifically designed for corporations operating in Louisiana. It covers both the Louisiana Corporation Income Tax and the Louisiana Corporation Franchise Tax. This form must be filed annually by corporations to report their income and calculate the taxes owed to the state.

Any corporation that does business in Louisiana or has income sourced from Louisiana is generally required to file the CIFT 620 form. This includes both domestic and foreign corporations that meet certain criteria. If your corporation has no taxable income or is not subject to franchise tax, you may not need to file, but it’s always good to check with a tax professional.

For corporations operating on a calendar year, the CIFT 620 form is due on April 15. If your corporation operates on a fiscal year, the due date will depend on the end of your fiscal year. Always refer to the specific instructions for your fiscal year to ensure timely filing.

To complete the CIFT 620 form, you will need various pieces of information, including:

Gathering this information beforehand can streamline the filing process.

Filing the CIFT 620 form late can result in penalties and interest on any unpaid taxes. The penalties can vary based on how late the form is filed. It’s important to file on time to avoid these additional costs. If you anticipate a delay, consider filing for an extension to mitigate penalties.

Yes, you can amend your CIFT 620 form if you discover errors or need to make changes. To do this, you must mark the appropriate circle on the form indicating that it is an amended return. Attach any necessary documentation that supports your amendments. Always keep a copy of the original and the amended return for your records.

If your corporation has no income to report, you may still be required to file the CIFT 620 form, especially if you are subject to franchise tax. Even if there is no tax due, filing a return ensures compliance with state regulations. Always consult the instructions for guidance based on your specific situation.

The completed CIFT 620 form should be mailed to the Louisiana Department of Revenue at the address specified on the form. Be sure to send it well in advance of the due date to ensure it is received on time. Avoid sending cash; use a check or money order for any payments due.

If you have questions about completing the CIFT 620 form, you can contact the Louisiana Department of Revenue directly. They offer resources and assistance for corporations filing their taxes. Additionally, consulting with a tax professional can provide personalized guidance tailored to your corporation's needs.

Filling out the Louisiana CIFT 620 form can be a complex process, and mistakes can lead to delays or complications. One common error is failing to provide the correct Louisiana Revenue Account Number. This number is crucial for the Louisiana Department of Revenue to identify your corporation accurately. Without it, your return may not be processed correctly, potentially leading to penalties or additional scrutiny.

Another frequent mistake involves incorrect reporting of federal taxable income. It is essential to ensure that the amount reported in Section B is accurate and reflects the corporation's true income. Miscalculating this figure can result in overpayment or underpayment of taxes, which may have serious financial implications. Always double-check your calculations and consider consulting with a tax professional if you are unsure.

Additionally, many individuals overlook the importance of including all required schedules with the CIFT 620 form. For instance, if you are required to submit the CIFT-620A, Apportionment and Allocation Schedules, failing to do so can lead to the rejection of your return. It is vital to review the instructions carefully and ensure that all necessary documentation is attached before submission.

Finally, neglecting to sign and date the return is a common oversight. This step is not merely a formality; it signifies that the information provided is accurate to the best of your knowledge. Without a signature, the return may be considered incomplete, which can further complicate your tax obligations. Taking the time to review your form thoroughly can help avoid these pitfalls and ensure a smoother filing process.

This is not true. The CIFT-620 form is required for all corporations operating in Louisiana, regardless of size. Small businesses must also comply with this tax filing requirement.

Filing the CIFT-620 form is mandatory for corporations that meet certain criteria. Failing to file can result in penalties and interest on unpaid taxes.

Corporations must file the CIFT-620 form by April 15 for calendar year returns. There are specific deadlines for fiscal year returns as well.

While profits are taxed, corporations can also account for losses. The form allows for loss carryforwards and carrybacks, which can reduce taxable income in future years.

The CIFT-620 form is specific to Louisiana and has different requirements than federal tax returns. Corporations must complete both forms separately.

Not all corporations are required to pay franchise tax. Some entities may be exempt based on their specific circumstances or structure.

While some may find it straightforward, the form can be complex. Proper attention to detail is necessary to avoid errors that could lead to audits or penalties.

Help is available through various resources, including the Louisiana Department of Revenue's website, tax professionals, and accounting firms that specialize in corporate tax filings.

| Fact Name | Details |

|---|---|

| Form Purpose | The Louisiana CIFT-620 form is used for filing both the Corporation Income Tax Return and the Corporation Franchise Tax Return for corporations operating in Louisiana. |

| Filing Deadline | Corporation tax returns must be filed by April 15 for calendar year entities. Fiscal year entities should refer to specific instructions for their deadlines. |

| Governing Laws | This form is governed by Louisiana Revised Statutes Title 47, specifically sections related to corporate income and franchise taxes. |

| Amendments | Corporations can mark a circle on the form to indicate if they are submitting an amended return, which may be necessary for corrections. |

| Information Required | The form requires details such as federal employer identification number, federal taxable income, and gross revenues, among other financial information. |

| Attachments | Schedule CIFT-620A, Apportionment and Allocation Schedules, must be included if applicable, along with any other necessary schedules for accurate reporting. |