Blank Louisiana R 6922 PDF Form

Blank Louisiana R 6922 PDF Form

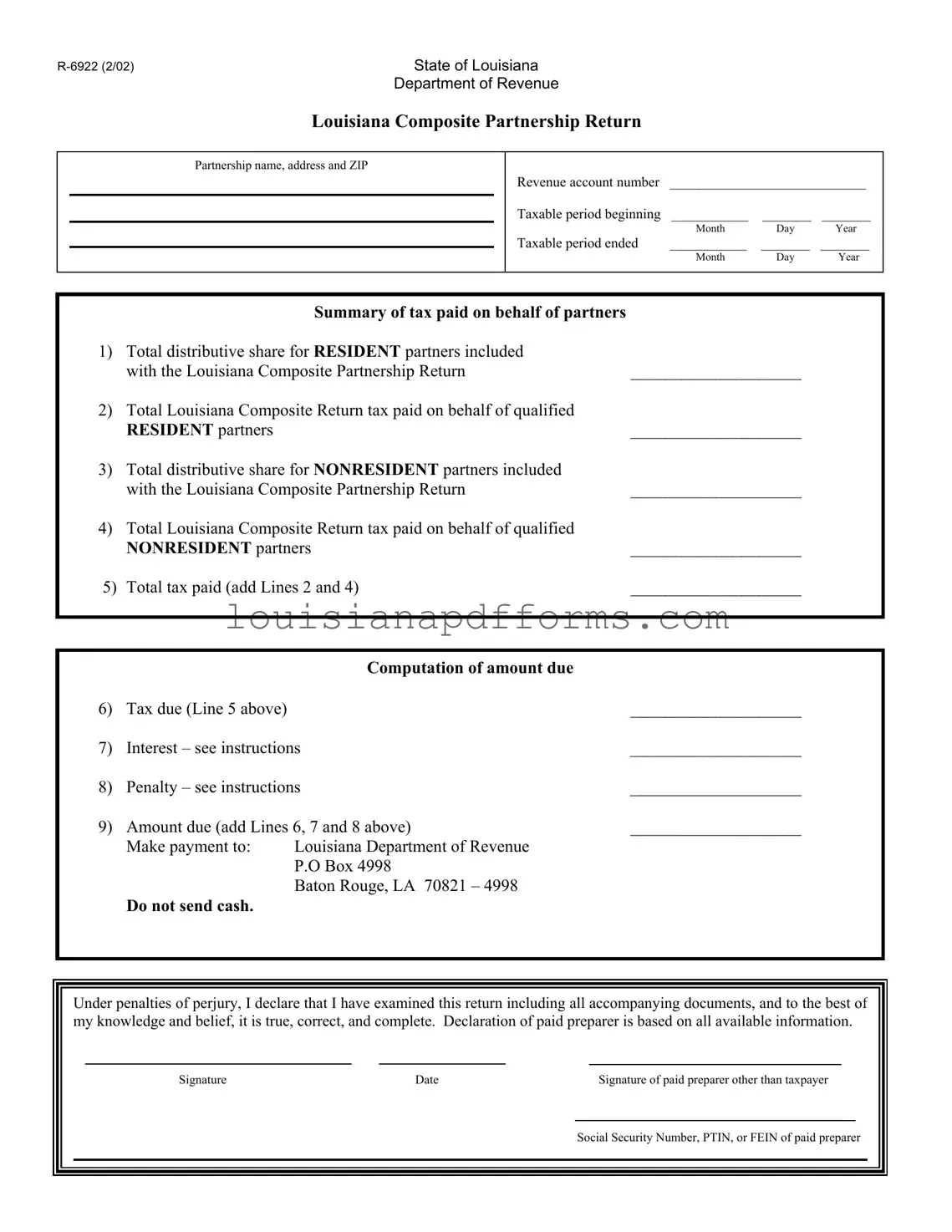

The Louisiana R 6922 form serves as a crucial document for partnerships operating within the state, specifically designed to facilitate the filing of taxes for both resident and nonresident partners. This form is a composite partnership return that simplifies the tax process by allowing partnerships to report and pay taxes on behalf of their partners, thereby streamlining compliance with Louisiana's tax regulations. It includes essential sections where partnerships must provide their name, address, and revenue account number, as well as the taxable period for which the return is being filed. The form breaks down the tax obligations into clear categories, such as total distributive shares for resident and nonresident partners, along with the corresponding taxes paid on their behalf. Additionally, it outlines the computation of the total amount due, incorporating any interest or penalties that may apply. By requiring signatures and declarations from both the taxpayer and the paid preparer, the R 6922 form ensures accountability and accuracy in tax reporting. This form not only helps partnerships meet their tax obligations but also plays a vital role in maintaining transparency and compliance within Louisiana's tax system.

State of Louisiana |

|

|

|

|

|||||

|

|

|

Department of Revenue |

|

|

|

|

||

|

|

|

Louisiana Composite Partnership Return |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

Partnership name, address and ZIP |

|

|

|

|

|

||

|

|

|

|

|

Revenue account number |

____________________________ |

|||

|

|

|

|

|

Taxable period beginning |

___________ |

_______ |

_______ |

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

Month |

Day |

Year |

|

|

|

|

|

Taxable period ended |

___________ |

_______ |

_______ |

|

|

|

|

|

|

|

|

Month |

Day |

Year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

Summary of tax paid on behalf of partners |

|

|

|

|

||

1) |

Total distributive share for RESIDENT partners included |

|

|

|

|

||||

|

|

with the Louisiana Composite Partnership Return |

____________________ |

|

|||||

2) |

Total Louisiana Composite Return tax paid on behalf of qualified |

|

|

|

|

||||

|

|

RESIDENT partners |

|

|

|

____________________ |

|

||

3) |

Total distributive share for NONRESIDENT partners included |

|

|

|

|

||||

|

|

with the Louisiana Composite Partnership Return |

____________________ |

|

|||||

4) |

Total Louisiana Composite Return tax paid on behalf of qualified |

|

|

|

|

||||

|

|

NONRESIDENT partners |

|

|

|

____________________ |

|

||

5) |

Total tax paid (add Lines 2 and 4) |

____________________ |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

Computation of amount due |

|

6) |

Tax due (Line 5 above) |

|

____________________ |

7) |

Interest – see instructions |

____________________ |

|

8) |

Penalty – see instructions |

____________________ |

|

9) |

Amount due (add Lines 6, 7 and 8 above) |

____________________ |

|

|

Make payment to: |

Louisiana Department of Revenue |

|

|

|

P.O Box 4998 |

|

|

|

Baton Rouge, LA 70821 – 4998 |

|

Do not send cash.

Under penalties of perjury, I declare that I have examined this return including all accompanying documents, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of paid preparer is based on all available information.

Signature |

Date |

Signature of paid preparer other than taxpayer |

Social Security Number, PTIN, or FEIN of paid preparer

State of Louisiana

Department of Revenue

Louisiana Resident Composite Tax Return Schedule

Partnership name ____________________________ |

Page _____ of _____ |

Revenue account number______________________ |

|

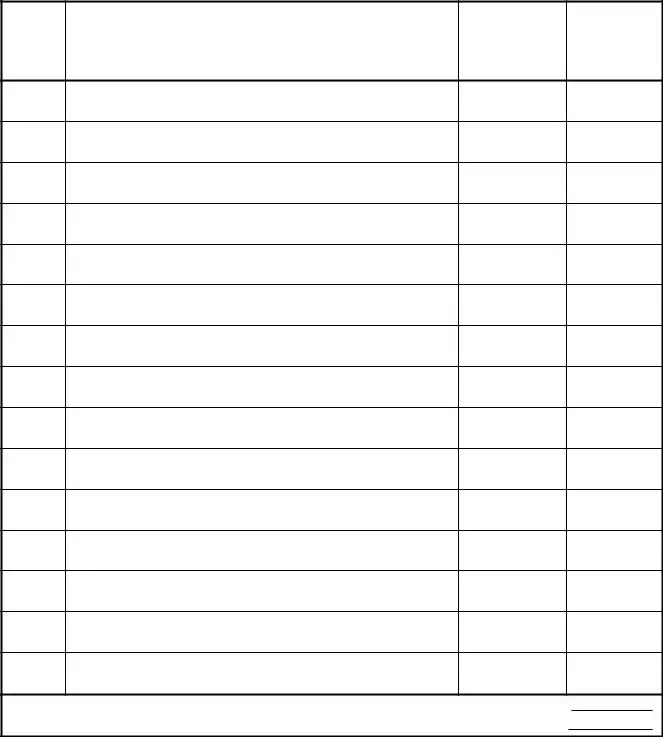

Partner Number

Name and address of partner

Partner ID

number

Distributable

share

Total distributive share for resident partners included with the Louisiana Composite Return…………………

Total LA Composite Return Tax paid on behalf of qualified resident partners included with the LA Composite Return…..

State of Louisiana

Department of Revenue

Louisiana Nonresident Composite Tax Return Schedule

Partnership name ____________________________ |

|

Page ____ of ____ |

|||||||

Revenue account number______________________ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Non- |

|

|

|

Partner |

Name and address of partner |

Partner ID |

Distributable |

|

|

resident |

Included in |

||

Number |

number |

share |

|

|

partner |

Composite |

|||

|

|

agreement |

Return |

||||||

|

|

|

|

|

|||||

|

|

|

|

|

|

filed |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total distributive share for nonresident partners included with the Louisiana Composite Return………………. |

|

|

|

|

|

||||

Total LA Composite Return Tax paid on behalf of qualified nonresident partners included with the LA Composite Return…. |

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

When filling out the Louisiana R 6922 form, it’s essential to follow certain guidelines to ensure accuracy and compliance. Here are eight things to keep in mind:

Following these tips will help streamline the process and minimize potential issues with your Louisiana R 6922 form submission.

Deq Aac 2 - It serves to provide necessary details about the type of operation being performed, whether demolition or renovation.

The Texas Motor Vehicle Bill of Sale form is not only a crucial legal document for recording the transfer of ownership but also serves as a reliable reference for both parties involved. To ensure a hassle-free transaction, it's recommended to use a well-structured form, such as one provided by Fast PDF Templates, which helps capture all necessary details, including the buyer's and seller's information, vehicle identification number, and sale price.

Deq 641 581Cert - Identify the finding location by referencing nearby blocks or miles.

Filling out the Louisiana R 6922 form requires attention to detail and accurate information. This form is essential for partnerships to report their tax obligations on behalf of their partners. Follow these steps to ensure the form is completed correctly.

The Louisiana R-6922 form serves as a crucial document for partnerships filing their composite tax returns. However, it is often accompanied by several other forms and documents that provide additional information and support for the filing process. Understanding these related documents can help ensure compliance and accuracy in tax reporting.

By familiarizing yourself with these forms and documents, you can navigate the complexities of partnership tax filings in Louisiana more effectively. Each document plays a vital role in ensuring that all partners are accurately represented and that the partnership meets its tax obligations.

The Louisiana R 6922 form is a tax return specifically designed for partnerships operating in Louisiana. It allows partnerships to report income and taxes on behalf of both resident and nonresident partners. By filing this form, partnerships can simplify their tax obligations, ensuring that the appropriate taxes are paid on behalf of their partners. This form is particularly useful for partnerships that want to streamline their tax reporting process while complying with state tax laws.

Any partnership that has partners who are residents or nonresidents of Louisiana may need to file the R 6922 form. If the partnership earns income that is subject to Louisiana state taxes, it is essential to report that income accurately. Additionally, partnerships that choose to pay taxes on behalf of their partners, rather than requiring individual partners to file separately, must use this form. This filing helps ensure that all tax obligations are met efficiently.

The R 6922 form requires several key pieces of information, including:

Providing accurate and complete information is crucial to avoid delays or issues with the filing process.

Tax calculation on the R 6922 form involves several steps. First, partnerships must determine the total distributive share for both resident and nonresident partners. This includes calculating the total tax paid on behalf of qualified partners. Once these amounts are known, the partnership adds the tax amounts for resident and nonresident partners to find the total tax due. Additional considerations, such as interest and penalties, may also apply, which must be added to the total amount due. The final amount represents what the partnership must pay to the Louisiana Department of Revenue.

Once the R 6922 form is completed, it should be mailed to the Louisiana Department of Revenue. The appropriate mailing address is:

P.O. Box 4998

Baton Rouge, LA 70821 – 4998

It is important to note that cash should not be sent with the form. Partnerships should ensure that the form is submitted by the appropriate deadline to avoid any potential penalties or interest charges.

Filling out the Louisiana R 6922 form can be a straightforward process, but there are common mistakes that can lead to delays or complications. One significant error occurs when individuals fail to provide accurate partnership information. This includes the partnership name, address, and revenue account number. If any of these details are incorrect or missing, it can cause issues with processing the return.

Another frequent mistake is neglecting to correctly identify the taxable periods. The form requires specific dates for both the beginning and end of the taxable period. Miswriting these dates can lead to confusion and may result in penalties or interest charges. It is essential to double-check that the dates correspond to the actual period the return covers.

Additionally, many individuals overlook the importance of accurately calculating the total distributive share for both resident and nonresident partners. Miscalculations can lead to incorrect tax amounts being reported. It is crucial to ensure that these figures reflect the actual distributions made during the taxable period.

People often forget to include the total Louisiana Composite Return tax paid on behalf of qualified partners. This is a vital part of the form, as it directly impacts the total tax due. Failing to report this amount can lead to underpayment and subsequent penalties.

Another common error involves the computation of the amount due. Many filers mistakenly add the interest and penalty amounts incorrectly. It is important to follow the instructions carefully and ensure that all calculations are accurate to avoid any unexpected liabilities.

Signature requirements are also frequently overlooked. The form mandates that the taxpayer and any paid preparer sign the return. Failing to include these signatures can result in the return being rejected or delayed. It is advisable to confirm that all necessary signatures are present before submission.

Lastly, some individuals make the mistake of sending cash as payment. The form explicitly states not to send cash, yet this is a common oversight. Instead, payments should be made through checks or other acceptable methods as outlined in the instructions. Following these guidelines can help ensure a smoother filing process.

Understanding the Louisiana R 6922 form can be challenging. Here are some common misconceptions that often arise:

Being aware of these misconceptions can help partnerships navigate their tax responsibilities more effectively. It’s always a good idea to consult with a tax professional if there are any uncertainties.

| Fact Name | Fact Description |

|---|---|

| Form Purpose | The Louisiana R-6922 form is used for filing a Composite Partnership Return, allowing partnerships to report income and taxes on behalf of their partners. |

| Governing Law | This form is governed by the Louisiana Revised Statutes, particularly Title 47, which outlines the state's tax regulations. |

| Taxable Period | The form requires the partnership to specify the taxable period, including the start and end dates for accurate reporting. |

| Resident Partners | It includes a section to report the total distributive share for resident partners, ensuring that their income is properly accounted for. |

| Nonresident Partners | The form also has provisions for reporting the distributive shares of nonresident partners, addressing their tax obligations in Louisiana. |

| Composite Tax Calculation | Partnerships must calculate the total tax paid on behalf of both resident and nonresident partners, which is summarized in the form. |

| Payment Instructions | Payments should be made to the Louisiana Department of Revenue, and cash is not accepted, ensuring secure transactions. |

| Declaration Requirement | The form requires a declaration under penalties of perjury, affirming the accuracy and completeness of the information provided. |

| Signature of Preparer | If a paid preparer assists in filing, their signature and identification number must also be included, adding an extra layer of accountability. |